The EUR-CHF exchange rate floor set by the Swiss National Bank (SNB) has indeed had the desired effect. Had the SNB not moved to set the floor, the euro would have fallen yet further. This is the conclusion drawn by an academic study conducted by Danish universities together with the University of Liechtenstein.

The EUR-CHF exchange rate floor set by the Swiss National Bank (SNB) has indeed had the desired effect. Had the SNB not moved to set the floor, the euro would have fallen yet further. This is the conclusion drawn by an academic study conducted by Danish universities together with the University of Liechtenstein.

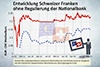

The SNB sprang into action on 6 September 2011, after the Swiss franc had almost reached parity with the euro during August of that year. In doing so, the SNB set an exchange rate floor of CHF 1.20 per euro and declared its commitment to buy unlimited quantities of foreign currency in order to achieve this goal. This move was made to protect the Swiss economy and has since proved itself to have been a successful strategy.

Successful SNB strategy

In order to assess how the EUR-CHF exchange rate would have developed without the intervention of the SNB, the experts used a model from the field of option pricing. The model was applied to forecast, inter alia, the latent, i.e. unobservable, exchange rate in the absence of the SNB’s exchange rate floor. An additional indirect finding of the study was the market’s confidence in the SNB’s commitment to this minimum rate, which was included as a factor in the results and determined from observable market data.

The researchers’ work initially showed that, relative to the actually observed exchange rate, the latent exchange rate would also have increased following the SNB decision, but would have fallen to CHF 1.10 per euro at the end of 2011. Without the SNB’s intervention, in 2012 the exchange rate would have stood at between CHF 1.05 and 1.10 to the euro, and therefore would have permanently been below the floor of CHF 1.20. A slight uptrend would have been observed in 2013, but the exchange rate would not have surpassed CHF 1.15 per euro. The exchange rate would then have stabilised at this level in the second half of 2013.

As is the case with the observable exchange rate, various events in the Eurozone can be easily identified in the development of the latent exchange rate calculated in the study. These include the negative developments in Greece and Italy at the end of 2011, followed by the downgrading of nine Eurozone countries by the ratings agency Standard & Poor’s. This move expressed the lacking confidence of the financial markets in the ability of European institutions to deliver solutions and pushed the exchange rate towards the floor of 1.20, from which it hardly moved during the second and third quarters of 2012. Likewise, the EUR-CHF exchange rate was primarily influenced and driven by events in the Eurozone throughout the period under review.

Professor Michael Hanke from the University of Liechtenstein, one of three authors of the study, summarises the findings as follows: “Without the intervention of the SNB, 2012 would have been far more difficult for export-oriented companies than it was anyway.”

Market confidence in the SNB

As the study also revealed, market expectations regarding the duration of the SNB’s commitment to the exchange rate floor changed considerably during the period reviewed. While the expected remaining duration of the SNB intervention was five months in November 2011, this figure had increased to nine months by the end of 2013. This is a reflection of the market’s increasing confidence in the commitment of the SNB.

For Professor Michael Hanke, it is clear that “the confidence of market participants in the ability of the SNB to maintain the announced exchange rate floor of 1.20 has been a key factor in ensuring the success of this measure.”

A summary of the findings can be found online at http://ssrn.com/abstract=2368698.